Strategy Updates

TACTICAL STRATEGIES

PREMIER WEALTH TACTICAL & PREMIER WEALTH TACTICAL CORE

Concerns about inflation, interest rates, and the debt ceiling have seemingly been brushed aside as investors rushed towards the Mega Cap Tech stocks chasing the allure of the AI revolution. Markets have managed to climb the proverbial wall of worry and make new highs for the year on both the NASDAQ and the S&P 500.

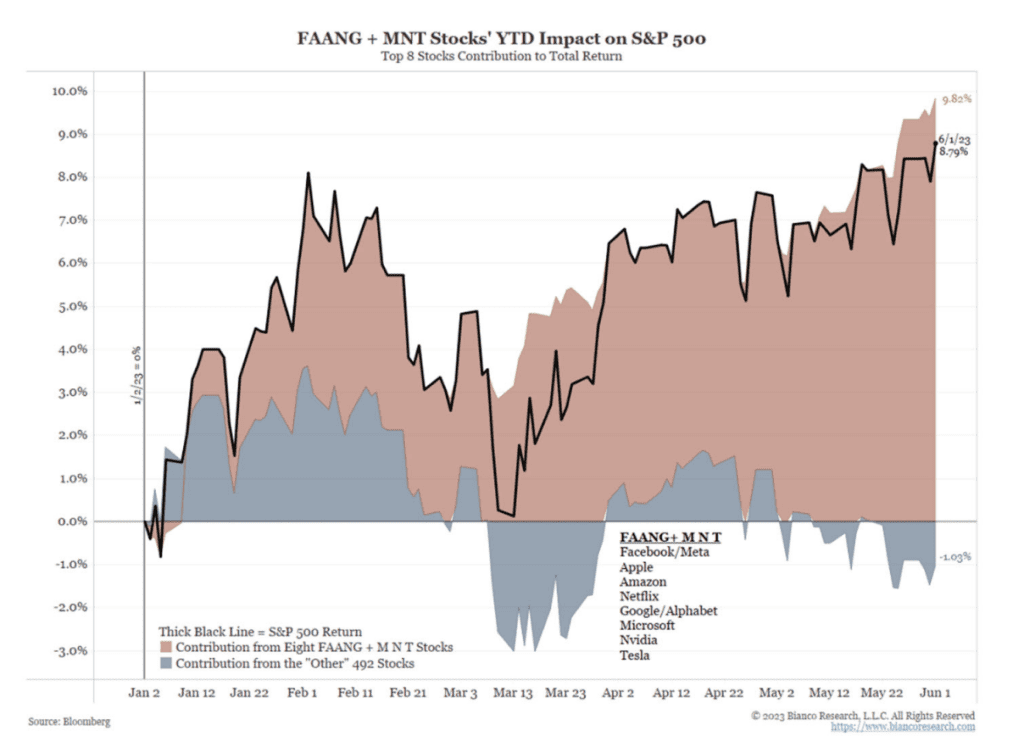

While the action in the market has been positive over the past month, one concern is the very narrow participation via Mega Cap Tech, especially AI and software companies. Through the end of May, the leadership was so narrow that the top 8 stocks by market capitalization on the S&P 500 accounted for a 9.8% return for the index. Since the S&P500 was only up 8.79% up to that point, that means the bottom 492 stocks in aggregate accounted for a 1% loss.

Historically, narrow markets are suspect, but we also know that these conditions can last a long time like we saw in the dotcom bubble. The good news is that we did see an expansion in participation as the S&P 500 broke out and made new highs last week.

Fundamentally, the combination of much better than expected earnings and the resolution of the debt ceiling appeared to be the catalyst that gave the markets the momentum to reach new highs. The messaging from the Fed that a pause in rate hikes in June likely contributed to that.

We have moved to increase our exposure and should things broaden out, more could be warranted. Some things to keep in mind is that some backing and filling should be normal, especially after the torrid run the NASDAQ has had.

In the intermediate term, the resolution of the debt ceiling means that the US will be issuing a massive amount of treasuries over the next few months. Some estimates are for more than 1 trillion before the third quarter. That would suck some liquidity out of the market.

In addition, student loan repayments are to be reinstated by September, likely reducing aggregate demand as what was temporary disposable income is forced back into paying debt.

Outside of the short term, markets will likely continue to be dictated by inflation and the Fed’s actions to fight it. While a pause is at hand, the Fed could be forced to do more if inflation doesn’t come down as expected. The strong jobs numbers we saw last week affirmed a strong labor market, which could keep inflation stickier than anticipated. In all, the technical action looks good but some caution is still appropriate as there is a confluence of factors that can still trip up this market later down the line.

TACTICAL OPPORTUNITY

Tactical Opportunity added some exposure as the market showed some life. The best month came in a rebound from AMZN, while several other stocks also had nice months. The narrow market makes it difficult to find buy signals, but we will add as they appear.

FULLY INVESTED STRATEGIES

ETF SECTOR ROTATION

The Growth sectors pressed their lead for the year with big moves over the last month in Tech (+9% vs a +3% S&P) and Consumer Discretionary (+9%). Communications (+5%) also had a good run. Outside of that, the picture was not pretty. Defensive plays Healthcare (-3%) and Consumer Staples (-6%) were the biggest laggards. Our model remains leaning toward the middle with overweights in Tech, Communications, and Energy. The action during the month saw us reduce our Healthcare exposure to an underweight.

In the broad markets, Growth posted a +6% month compared to a negative one for Value. Small Caps outperformed and Internationals lagged. Currently, we still hold exposure in Europe, but not Emerging Markets.

EQUITY GROWTH OPPORTUNITY

The market found its footing in May, led by the resurgent Technology sector. The broad indices appear to be following suit, which is increasing our optimism. We are continuing to explore increasing the beta in the portfolio to take advantage of this upswing.

EQUITY GROWTH AND VALUE

No surprise here as Tech holdings had outsized runs since May 1, such as Advanced Micro, Applied Materials, Nividia, and Broadcom. Also, as expected, defensive names lagged, though most not too badly. Normal rotating is expected to occur as the market decides if the Growth run will last.

EQUITY DIVIDEND INCOME

With Growth getting the headlines, the more value minded dividend stocks lagged, and as a group were down slightly. Healthcare and Staples stocks declined as money rushed for AI names. Not abnormal behavior for a dividend group. Normal activity expected.

RISK BLENDED STRATEGIES

Our Risk Blended Strategies are a combination of both Premier Wealth Tactical Core and ETF Sector Rotation. Please see the above commentary for more information on each strategy.

- Churchill Moderate: 70% Premier Wealth Tactical Core / 30% ETF Sector Rotation

- Churchill Moderately Aggressive: 50% Premier Wealth Tactical Core / 50% ETF Sector Rotation

- Churchill Aggressive: 30% Premier Wealth Tactical Core / 70% ETF Sector Rotation

For a full description of each strategy, please click here.

Best regards,

CHURCHILL MANAGEMENT GROUP

877-937-7110

[email protected]

** This report is meant to inform the reader of our current market opinion, which we, as professional money managers, use in our decision-making. It should be noted that stock market and bond market data are subject to varying interpretations and any one interpretation will not necessarily guarantee investment success. The information obtained from the sources specified herein and used as a basis for our current market opinion is believed reliable, but we do not guarantee the accuracy of such information. The references to specific investments were chosen based on our current market outlook, as examples representing how aspects of the market have performed and as representation of what a strategy might own. Those are included for informational purposes only and past specific investment advice does not guarantee future results.

TACTICAL STRATEGIES

PREMIER WEALTH TACTICAL & PREMIER WEALTH TACTICAL CORE

Despite concerns over inflation and earnings declines, stocks have been hanging tough. Markets rose a little over one percent in April. Are investors being too complacent or will the economy pull off the difficult soft landing in the face of tightening financial conditions?

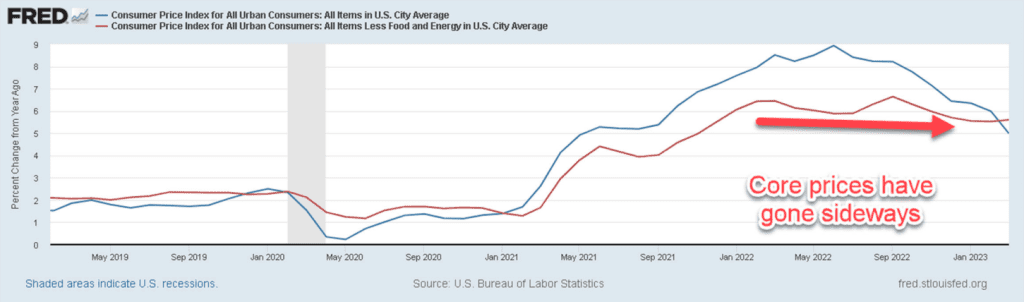

Inflation has been the chief concern for the economy. The good news is that inflation is clearly coming down from its high levels. However, core prices – the Fed’s preferred measure of inflation which excludes food and energy – has been stickier than hoped. This likely means the Fed Funds rate will remain higher for longer.

Meanwhile, corporate earnings are muted but maybe not as bad as initially feared. With 53% of the S&P 500 having already reported, 79% have beaten their earnings estimates while 74% have topped revenue targets. True, most of that is a function of lowered expectations, but some large-cap tech bellwethers delivered robust reports. Tech titans Microsoft, Alphabet, Meta, and Amazon powered through earnings, easily beating their targets. Apple will also be reporting this week- their results will surely be closely watched.

As a result, stock returns have been narrowly focused year to date. Large-cap Tech has carried the market with eight Mega cap stocks making up 6.44% of the 7.65% gain in the S&P 500 year to date. The other 492 stocks in the S&P 500, in aggregate, have gained a mere 1.21% this year.

On the economic front, the Fed recently raised rates 25bps and signaled that a pause could be at hand but that would depend on incoming data. Chairman Powell did also reiterate that the Fed does not see the conditions for rate cuts this year based on their current forecast. That is at odds with what the market has been pricing and could be a point of contention for markets. Higher rates have clearly put more pressure on the regional banks as depositors continue to move money out. The regional banks index made fresh lows this week. The likely reason is the rate differential between what these banks are paying their depositors and what they can get in money markets. On average they are paying half a percent when money market funds are yielding 4.5%.

Another potential market-moving economic release is Friday’s jobs report. A strong jobs number would affirm the Fed’s recent mantra of higher for longer in terms of rates while a weaker number would boost the case for a pivot happening sooner.

On a technical basis, the market highs seen back in February have acted as some resistance on the upside. A breakout above those levels would be a positive development.

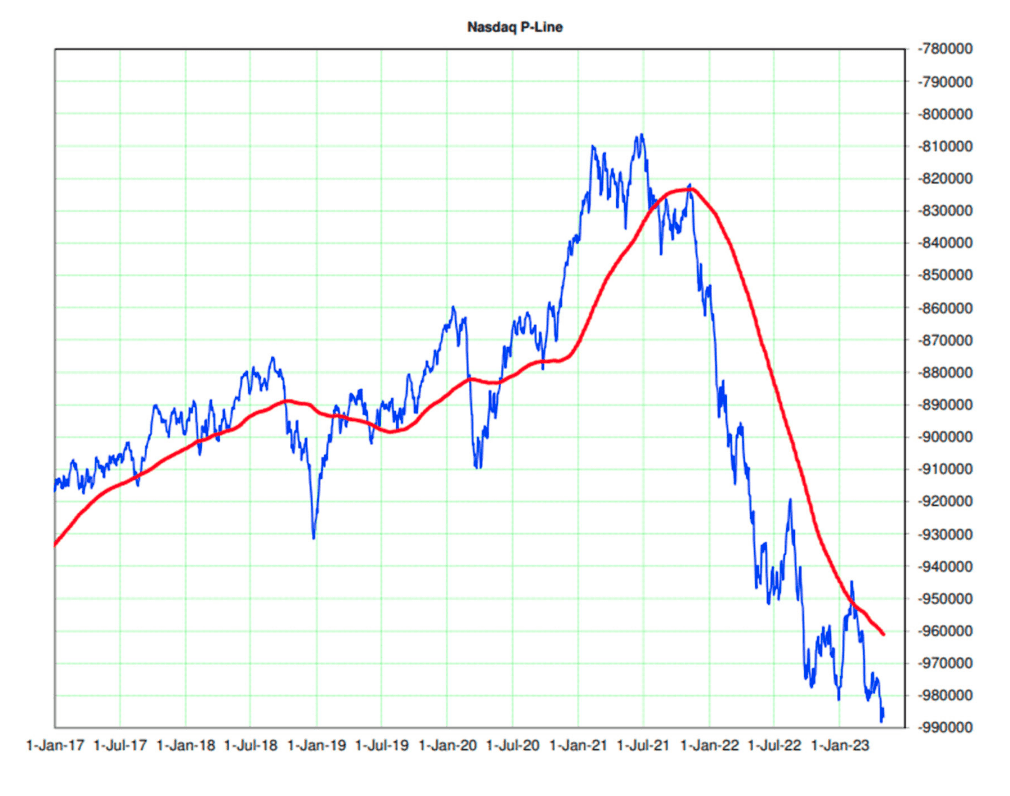

An area of concern is the top-heavy nature of the market mentioned above. Consider the breadth in the Nasdaq. The cumulative advance-decline line is currently sitting around the lows for this cycle. Markets are deemed to be much healthier when the vast majority of issues are participating.

While we have seen plenty of volatility over the last year, it is surprising to many that the S&P 500 trades around the same levels it was at this time in 2022. The indices have essentially traded sideways between 3600 and 4200. Hopefully, the long trading range turns out to be a classic bottoming process that historically follows a bear market before a recovery – unlike the V-shaped recoveries seen in recent years.

Whether it will ultimately be defined as a bottoming process will only be known in retrospect. However, for now, the back-and-forth action certainly gives hope for one. With the rest of earnings season rolling out in the next couple of weeks, including the behemoth in Apple, the market still faces some tests ahead.

TACTICAL OPPORTUNITY

Old school Tech stocks have been doing better than most as Microsoft, Apple, and Google are holding up well so far. Good earnings from Microsoft and Google have played a role in that. Apple’s earnings are on deck and could bolster the status quo if they can do the same. Until the market can establish an up or down trend with consistency, our percent invested will likely remain largely the same.

FULLY INVESTED STRATEGIES

ETF SECTOR ROTATION

Clear sector leadership remains elusive in 2023. Different sectors have taken the lead only to give it back shortly after. Energy has been lagging as of late with the price of oil having taken a hit. Outperforming over that past month have been Communications and Consumer Staples. We are overweight Tech, Healthcare, and Energy, with the latter getting a close look in the face of some recent weakness. It is not unusual for Energy to be a volatile trade. Despite bank headlines, the Financial sector has held up ok outside of regional banks.

The narrow market has been tough to beat, with the majority of sectors lagging. For broad markets, Growth and Value have been about the same over the last month. Small caps have hit some trouble and is behind the lagging market breadth numbers. Internationally, we are fully in on Europe and halfway on Emerging Markets.

EQUITY GROWTH OPPORTUNITY

The portfolio remained calm in April as we are on the lookout for leadership to emerge before making any major allocation changes. The tides have swayed from Growth/Technology to Value and now back to Mega-cap Technology with some strong earnings reports last week. The market is on the edge of resistance with the potential to break out of a year-long trading range. Should we get some upside momentum, we may look to increase the beta in the portfolio.

EQUITY GROWTH AND VALUE

Stocks are bumping around since the start of April with both winners and losers showing no real direction. Some energy and industrial names are paring back like Valero Energy and Carrier Global. On the other side, we had good months from names like Chipotle, Molson Coors, and Vertex Pharma. We will continue to look for some rotation opportunities as the market continues to look for its footing.

EQUITY DIVIDEND INCOME

Dividend paying stocks have been treading water in the face of some tough trading recently. Energy holdings have contributed to that as they are giving back some past gains. We have pared some holdings there. Consumer staple stocks had positive moves in recent weeks. No significant changes are expected.

RISK BLENDED STRATEGIES

Our Risk Blended Strategies are a combination of both Premier Wealth Tactical Core and ETF Sector Rotation. Please see the above commentary for more information on each strategy.

- Churchill Moderate: 70% Premier Wealth Tactical Core / 30% ETF Sector Rotation

- Churchill Moderately Aggressive: 50% Premier Wealth Tactical Core / 50% ETF Sector Rotation

- Churchill Aggressive: 30% Premier Wealth Tactical Core / 70% ETF Sector Rotation

Best regards,

CHURCHILL MANAGEMENT GROUP

877-937-7110

[email protected]

** This report is meant to inform the reader of our current market opinion, which we, as professional money managers, use in our decision-making. It should be noted that stock market and bond market data are subject to varying interpretations and any one interpretation will not necessarily guarantee investment success. The information obtained from the sources specified herein and used as a basis for our current market opinion is believed reliable, but we do not guarantee the accuracy of such information. The references to specific investments were chosen based on our current market outlook, as examples representing how aspects of the market have performed and as representation of what a strategy might own. Those are included for informational purposes only and past specific investment advice does not guarantee future results.

On December 29, 2022, President Biden signed into law the Secure Act 2.0. The Secure Act 2.0 contains over 100 legislative updates, with several that may have a meaningful effect on our clients. Some of these updates take place this year 2023, however, many are not effective until future years. Below is a summary of the more impactful changes.

Age Changes for Required Minimum Distributions (RMDs) – Effective 2023

Effective January 1, 2023, the RMD age increases to 73 from 72. RMD age increases again to age 75 for those born in the year or after 1960. If you are already of RMD age you will not be able to postpone your RMD.

Qualified Charitable Donations (QCD) age is not impacted, it remains age 70.5 for QCDs.

Reduced Penalties for Required Minimum Distributions (RMDs) – Effective 2023

SECURE 2.0 Act reduces the penalty for missing an RMD from a 50% penalty down to a 25% penalty. Under some circumstances, the penalty can be reduced further to a 10% penalty if fixed during the Correction Window outlined in the Secure Act 2.0.

New Roth Retirement Account Options – Effective 2023

Both SEP IRAs and SIMPLE IRAs will now be able to accept Roth contributions.

New Roth Employer Contribution Allowance – Effective 2023

For both employer matching and non-elective contributions, employer Roth contributions may be allowable for qualified retirement plans.

New 529 Rules Allowing Balance to be Rolled into Roth IRAs – Effective 2024

Some 529 plans may be allowed to be rolled over to Roth IRAs. However, there are some limitations including the 529 account must be older than 15 years and the total lifetime rollover cannot exceed $35,000.

IRA Catch-up Contributions Now Tied to Inflation – Effective 2024

IRA catch-up contributions will soon be tied to inflation in $100 increments.

Larger 401(k), 403(b) and SIMPLE IRA Catch-up Contributions – Effective 2025

401(k) and 403(b) catch-up contributions for people ages 50 and older will increase to the greater of $10,000 or 50% more than the regular catch-up amount if you are 60, 61, 62, or 63 years old.

Expanded Access to Retirement Accounts For Special Circumstances – Effective 2023

Access to retirement for funds at age 50 without penalty now applies to certain employees such as firefighters and correction officers.This also applies to individuals who have worked at the same company for over 25 years.

Access to retirement funds without penalty has expanded to individuals in qualified Federal disaster areas. Repayment is required within three years.

Access to retirement funds without penalty has expanded to individuals with a terminal illness. Terminal illness is now expanded to 84 months. Repayment is required within three years.

Talk to your Churchill advisor for more details on how to maximize your retirement accounts and work with your tax preparer for tax planning and final tax advice.

Summarized by Director of Financial Planning: Scott Perkins, MSTax, MBA, CFP®