News

For the third year in a row, Churchill Management has been named to the 2020 edition of the Financial Times 300 Top Registered Investment Advisers.* The list recognizes top independent RIA firms from across the U.S.

In compiling its list of elite RIA firms, Financial Times evaluated firms based on their assets under management growth, years in existence, industry credentials of advisers, and compliance records.

“At Churchill Management we believe that close personal attention and a commitment to building wealth over the long term is key to helping client’s achieve their personal and financial goals,” said Randy Conner, President of Churchill Management Group. “We appreciate that Financial Times has acknowledged our dedication to this goal.”

We would be happy to help you in this volatile time with a complimentary financial review. You may contact us at (877) 937-7110 or [email protected] or feel free to click here to schedule a complimentary financial review.

As with most things in life, timing is everything when it comes to retirement. Sequence of Return Risk is the danger that the timing of withdrawals from retirement accounts will have a negative impact on the overall rate of return and assets available to an investor. Retire in a bull market and you will probably be enjoying life, but retire in a bear market and the picture might not be so rosy. Since we can’t predict the future it’s important to be prepared for whatever market you encounter during retirement. Below we discuss the Investor Lifecycle, what it means, and how you can avoid sequence of return risk and enjoy the retirement you deserve.

The Investor Lifecycle

The Investor Lifecycle is comprised of three distinct phases. Phase one is known as the Accumulation Phase. In this phase, typically lasting 35-40 years, you focus on growth for the future. The Preservation Phase, Phase Two, is when you prepare for retirement. During this phase, it becomes more and more prudent to reduce risk taking and increase your participation in protective investment strategies. The third and final phase is the Distribution Phase. This period of a person’s life is where they will transition from earning their income to taking it in large part from their retirement savings. This phase is critical to examine because at this point there is no attractive way of turning back should something go awry.

The Sequence of Return Risk: The Importance of Timing

During the Distribution Phase, it is especially important to be aware of Sequence of Return Risk. As a reminder, Sequence of Return Risk is the risk that the timing of withdrawals will have a negative impact on your portfolio’s value. It is specifically down markets that have a significant impact on a retiree who depends on taking income from their investments because they are withdrawing funds from a continuous shrinking pool of assets. The return needed to recover these losses grows as losses mount.

For example, imagine you retire at the beginning of the 2000 Bear Market with $1 million invested in the S&P 500. You plan to take out $50,000 a year and increase your withdrawal by 3% every year for inflation. The bad news is your nest egg would be gone by 2016. However, if you replace those terrible years from 2000-2002 with 2014-2016 it is a completely different story. Today your portfolio would still be over $1 million vs $0 in 2016.

How to Mitigate Sequence of Return Risk

The good news is you don’t have to let the market determine whether you spend your retirement on a beach or worried about paying bills. There are a number of ways you can limit the damage of sequence of return risk depending upon where you are in the Investor Lifecycle. Below we highlight some of the most common and the pros and cons of each.

Buy and Hold Strategy

In a buy and hold strategy, you buy stocks with the intent to hold on for the long-term. If you are in the early stages of the investor lifecycle, with lots of time on your hands, this strategy can offer returns with fewer headaches and can be great for taxes. However, if you lack time to make up any potential losses this strategy places you at the mercy of the market.

Use Bonds

Another common strategy is allocating a portion of your portfolio to bonds. In theory, the more bonds you have in a portfolio, the less volatility you will be exposed to in the market. However, remember that every decision in investing comes with a tradeoff. As you dial up the proportion of bonds in the portfolio, the tradeoff is a lower expected long-term return. In a declining interest-rate market, will that lower return be enough to cover your needs?

A Tactical Approach

A tactical approach aims to preserve capital during times of high risk through the use of cash and cash equivalents. The percentage of the strategy invested in the stock market may vary depending upon the prevailing risks in the market. This strategy can offer you reduced volatility and capital preservation during those critical distribution years but in rocky markets, you might occasionally miss some upside potential.

The Next Step

At the end of the day, the goal is not to beat an index but instead have a strategy in place that allows you to sleep at night and achieve your goals. Accomplishing these goals involves understanding where you are in your Investor Lifecycle and evaluating the trade-off between risk and return. Can you ride out the market in the hopes of superior returns? On the other hand, would you rather limit your risk and minimize losses? Once you have those answers, put your investment strategy into place.

About Churchill Management Group

Churchill Management Group was founded in 1963. Our Firm and/or Portfolio Managers have been named Barron’s #1 Top Independent Advisor in 2016 and ranked #1 Best-in-State Advisor: CA – Los Angeles in 2020 and #13 on Forbes list of America’s Top 250 Wealth Advisors in 2019.* It is our mission to grow capital in favorable markets and protect in less favorable high-risk environments through our tactical strategies.

Find out More.

If you have $500,000 or more in investable assets and would like a complimentary financial review, please contact us at [email protected] or (877) 937-7110 or click here to schedule a complimentary financial review.

Why does it seem like there is such a huge disconnect between the economy and the stock market?

With global lockdown orders, economies closed for business, and oil hitting historic lows, the U.S. stock market is only down 17% from the all-time high of February 19th. This is after going through a bear market (down 20% from the recent high) in 16 trading days, the fastest 20% drop in history. The market then continued to roll over and was down over 35% by March 23rd. Also being questioned is whether we will see an L-shaped reset, a slower U-shaped formation, or a fast V-shaped recovery. My favorite show, Wheel of Fortune, allows a contestant three consonants and one vowel in the final puzzle, so let’s throw in a W-shaped reset (a quick recovery followed by another decline) for good measure. Hopefully, we have enough letter-based clues to have any insight on how the future recovery may play out.

Breaking Down the Economy

Before we try to solve the puzzle, we must understand that the most common indicator to track the health of a nation’s economy is Gross Domestic Product (GDP), the sum of goods and services, all of the things we produce. Government spending, business investments, and consumer spending on the goods and services produced within the economy all contribute to the GDP growth of the country. The economy is what is happening in real-time, what we all are experiencing now. The pandemic has and will continue to impact our economy and the road to recovery will be one that happens in real-time. Over 30 million Americans have filed for unemployment since mid-March, causing real unemployment rates to skyrocket past 20%, ultimately wiping out 10 years of job gains. Interest rates are also at historic lows and most analysts expect our economy (GDP) to contract in the second quarter between 8-24%. Without a doubt, these are catastrophic numbers and nothing to discount considering the impact for years to come on individuals and the industries that shape our current way of life. Breaking Down the Market The term “stock market” often refers to one of the major stock market indices, such as the Dow Jones Industrial Average or the SP 500 which many investors utilize as a benchmark to measure risk and reward. The SP is widely thought of as the best representation of the U.S. stock market. Stock prices are forward-looking in the sense that investors buy and sell stocks not based on what happened yesterday or what is happening today, but rather based on their expectations for the future, usually over the next 3-30 months. A bear market has lasted on average18 months. However, what happens in a bear market can have a multiyear impact on your recovery. Keep in mind it took seven years to get back to the 2000 highs in 2007. It also took five-and-a-half years to get back to the 2007 highs in late 2012. When you are down 50%, you will need 100% return just to get back to even. Over the past month, the stock market started to negatively price in a recession (traditionally being defined as two consecutive quarters or six straight months of negative economic growth) and more recently stocks have risen on the dismissal of pandemic fears and the hope of a quick economic recovery and a return to business as quasi-usual.

The Economy vs. The Market

The stock market and the economy are certainly related, but they do not rise and fall in sync. This is not to say the economy does not impact the stock market, however, one major fallacy is the belief that when the economy is contracting, stock market returns, in turn, will drop. Historically, GDP is not a good predictor of future stock prices and quite the opposite oftentimes has occurred.The stock market has tended to peak prior to the onset of a recession, and trough before the end of a recession. Therefore, we believe it is important to understand what the shape of the economic recovery means for the markets as this is influential to our investment approach.

Solutions Available to You

This pandemic has impacted everyone in their own personal way and I am sure most investors hope to never hear again phrases like “welcome to the new normal” and “unprecedented uncertainty.” During this crisis, and even more so than the financial crisis of 2008, I have realized how investors are consumed by the daily market fluctuations and the mental, emotional, and even physical toll it has taken on them. Investor panic is a natural response and to battle a “flight or fight” response to that would be futile. Although now has been a better time than ever to practice emotional distancing with your investments, it is not the time to “stay the course,” “hang in there” and do nothing. If that were so simple, in 2001, Dalbar, a financial-services research firm, would not have concluded that average investors fail to achieve market-index returns. It found that in the 17-year period to December 2000, the SP 500 returned an average of 16.29% per year, while the typical equity investor achieved only 5.32% for the same period – in other words a severe underperformance. It is however, the time to work with a professional money manager who understands every individual is not, and should not be on the same course, especially a crash course. Every investor has their unique needs and goals and deserves a solution that not only gets you to your goals, but in a way that is comfortable to you. That is why Churchill Management Group utilizes a blend of our unique tactical strategies that manage risk through equity exposure combined with our fully invested strategies that are actively managed in a strategic way toward leadership and new opportunities.

Don’t Stay the Course, Chart Your Course

I recommend having a portfolio that adjusts to the changes that come so you do not have to make changes, like cutting expenses, going back to work, or delaying your dreams because now you are forced to wait and recover. What is the point to even discuss what type of economic or stock market recovery we will see if “staying the course” is the answer? The stock market and the economy are not the same and for many conventional investment strategies, LUV, or any other shape has got nothing to do with it.

Find out More.

If you have $500,000 or more in investable assets and would like a complimentary financial review, please contact us at [email protected] or (877) 937-7110 or click here to schedule a complimentary financial review.

As if the coronavirus pandemic fears weren’t bad enough for stocks, the news over the weekend of the collapse of the OPEC+ deal made matters worse. News broke Sunday of an all-out price war involving Saudi Arabia and Russia, and overnight oil prices fell 30%. Stocks took the news hard, tumbling 7% to start the day today, triggering a trading circuit breaker on the exchange. By the end of the day, every index was off by more than 7%. This is probably not the way the stock market wanted to celebrate the 11th anniversary of the end of the financial crisis which bottomed March 9, 2009.

The markets have spent the past two-plus weeks in an area of extreme uncertainty where much is unknown. The market does not like uncertainty and the unknown.

The most pressing and unavoidable of the unknowns have been, of course, the coronavirus. How many people will be impacted? How long will it last? How much will it cost in terms of economic impact? No one really knows for sure. It seems everyone is assessing their own personal situation and asking if they are over or under-reacting.

As a result of the unknown, market volatility has been off the charts. Last week, all five trading days saw a move of greater than 2%. In what might come as a surprise, the market was actually UP last week thanks to a couple of strong bounces during the week.

Due to the uncertainty and volatility, we have continued to reduce our stock market exposure in our tactical strategies. We expect the market to remain choppy as it tries to figure out what the economic fallout will be from the virus fears, and now the oil issues. That volatility can include sharp rebounds as fears turn to hopes. We expect the Fed will be aggressive, though it is unlikely further rate cuts to already historically low rates will have much impact on virus fears, or oil wars for that matter. More helpful, and probably likely, will be targeted fiscal policy that attempts to help cash crunches caused by the turmoil. In all events, we expect there to be a process that takes some time, whether things continue to get worse or start to recover.

So far, the speed of this decline has been highly unusual. The stock market was at all-time highs just nineteen days ago. It now sits just a whisper from Bear Market territory, which is defined as a drop of 20% from the highs. The quickest 20% decline ever happened back in 1929 when it took just 42 days. During the 2008 financial crisis, it took 274 days or almost nine months.

If we are heading toward a significant Bear Market, like the one we saw back in 2008 for example, we would still be early in both terms of time and drawdown. In 2008, the market hit the total decline we reached today in mid-March of 2008, a full year before the bottom and with some 35% plus still to go on the downside.

To summarize, we have thus far taken multiple steps to raise cash and protect within our tactical strategies while also remaining prepared for any bounce which can be captured through our multi-strategy experience. We will continue to monitor the markets diligently and act accordingly.

Best regards,

CHURCHILL MANAGEMENT GROUP

877-937-7110

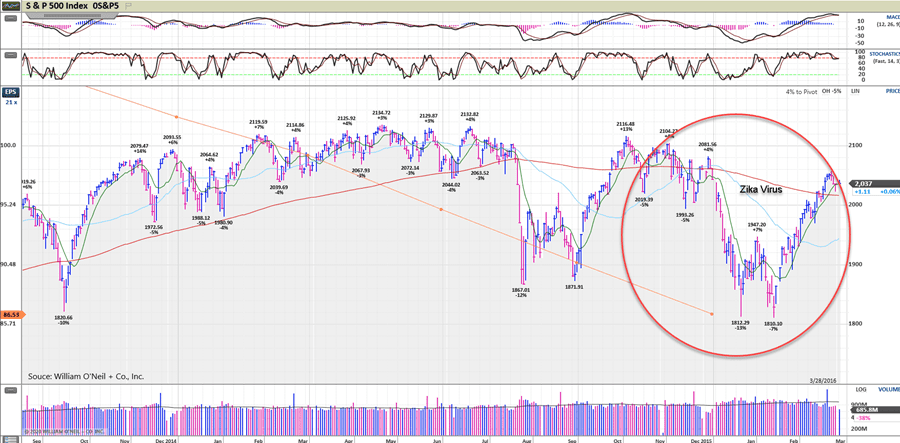

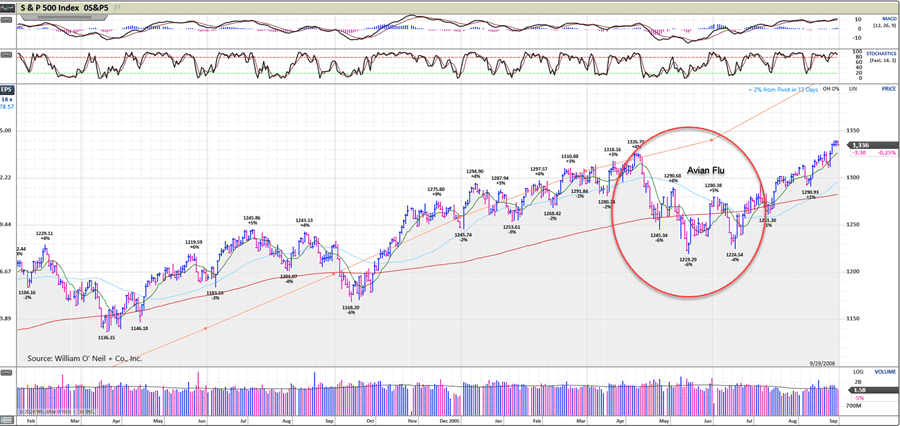

Volatility struck the markets as news over the weekend spread of new coronavirus cases outside of China, namely in South Korea and Italy. The reaction has been sharp and swift but that is a common reaction based on past epidemics.

For example, if we take a look at previous epidemics such as the Zika Virus and Avian Flu we see a similar pattern. The sell-off is sharp but short-term.

At this point, markets have come straight off their highs and have become oversold quickly. We are now down 7.5% on the S&P 500, only 5 days removed from all-time highs. Based on the extreme readings, the expectation is that we should see an oversold bounce at some point with both the 200 day moving average and the November breakout within reach on the S&P 500. Those areas should act as support.

We will know much more about the nature of the sell-off based on how it reacts on the bounce. Even if we have seen the ultimate top, history tells us that topping is a process and that there will be opportunities to make adjustments down the line. We will continue to watch the situation very closely.

Have Questions? Ask the Experts.

Contact your Churchill Representative to ask for an opinion on a stock, an analysis on your outside portfolio, or even just a general question on the market.

(877) 937-7110

As 2020 and the Presidential election loom on the horizon, many investors may feel a certain amount of unease. Elections can bring with them explosive headlines and a general sense of unpredictability. This may be more compounded in today’s world where it seems that a Presidential tweet can send the market up or down. However, do these fears warrant a drastic change to your portfolio?

What Can History Tell Us?

If you take a look all the way back to 1928, 82% of the time the S&P 500 has ended the year positive during an election year. The average return for all the election years going back to 1928 is just over 11% and averaged almost 17% for the positive years. Looking back to our two last election years in 2016 and 2012 the S&P 500 achieved returns of 12% and 16% respectively. Not too shabby or a reason to run for the hills.

Do’s and Don’ts

First, the don’ts – don’t put too much weight on headlines, current events, and widely expected occurrences. More than likely the market has already priced in these factors. You could be damaging your long-term results by putting too much stock into these events.

Instead of making a guess on where the market is going in an election year, basing your decisions on emotions stirred up the media, we recommend you maintain a focused and disciplined approach. This means concentrating on your financial goals and / or needs, your risk tolerance, and time horizon.

A Great Time for a Portfolio Check-up

As we head into 2020 take some time to evaluate your current portfolio. It might prove a welcome distraction from the onslaught of election coverage! Is it aligned with your financial goals? Have your needs or time horizon changed? If not, it might be time for a portfolio check-up.

Find out More.

If you have $500,000 or more in investable assets and would like a complimentary portfolio check-up, please contact us at [email protected] or (877) 937-7110.

While the S&P 500 remains near an all-time high, investors are looking at their portfolios and asking, “if the market is at all-time highs, shouldn’t I be as well?” Not so fast.

While equity markets often move with some element of correlation, the last five years and especially the last one year has been truly exceptional. As of October 7, the one year return of the S&P is basically flat at 1.84%. Compare this to the Russell 2000 Small-Cap at -7.9%, International MSCI EAFE -3% and the Emerging Markets index -0.66%. If you extend this to five years the numbers are even more surprising with the S&P up a whopping 53.83%. Compare that to the EAFE 6.18%, and emerging markets 0.30%. The commodity index is down 33.69% over the last 5 years!

A Tough Ride for Diversity

For years, legions of investors have adopted the advice of noted passive index investors like Burton Malkiel and Jack Bogle. While both championed the benefits of passive “buy and hold” investing, both were also careful to advocate that investors create a truly diversified approach to investing. A thoughtful well-constructed portfolio might have consisted of Large Cap, Mid Cap, Small Cap, Bonds, International, Emerging Markets, Commodities, and many more categories. Neither would have advocated for a single country, single market cap approach to investing such as the S&P 500. Needless to say, for a thoughtful well-constructed portfolio, it has been a difficult period indeed!

Part of the story is playing out in the headlines today. The global economy is slowing. The IMF recently cut global GDP forecasts for 2019 and the recent strength in the U.S. dollar has sent shockwaves through the global bond markets. German government 10-year bond yields are at -0.57%! The U.S. Federal Reserve sensing the global implications made a significant reversal in policy by raising interest rates in December and yet lowering rates just seven months later.

Shockingly Large Cap Leads the Way

So where is this U.S. Large Cap outlier performance coming from? Surprisingly, these last five years have seen the largest of the large Cap lead the way. Of the 500 companies in the index, the five year returns of the top 8 companies are Microsoft +211%, Apple +125%, Amazon +456%, Google +117%, Facebook +146%, Berkshire Hathaway +51.54%, Visa +241%, Johnson & Johnson +31%.

Focus on Your Goals

In my 25 years of investing, I have largely ignored the phrase “it’s different this time”, perhaps this time it is. What should investors do instead? Instead of continuously chasing the S&P 500, investors should examine their individual goals and risk tolerance. Are they willing to take on the risks that come with achieving these returns by having a largely undiversified portfolio? Are they comfortable giving up some performance for reduced volatility? In these uncertain times, it may be better to leave a little on the table.

Have Questions? Ask the Experts.

Contact your Churchill Representative to ask for an opinion on a stock, an analysis on your outside portfolio, or even just a general question on the market.

(877) 937-7110

LOS ANGELES, Sept. 12, 2019 /PRNewswire/ — Churchill Management Group’s President, Randy Conner, jumped two spots to #13 on Forbes Magazine’s recently released list of America’s Top Wealth Advisors. Mr. Conner was also previously named the #1 Best-in-State Wealth Advisor for CA – Los Angeles by the magazine in 2019.

Read full article here.

THE MOST INFLUENTIAL WEALTH MANAGERS IN LOS ANGELES The right wealth management professional does more than advise you regarding how to invest your money. He or she – and the financial institutions they represent – can genuinely prepare your entire family for financial stability and fiscal comfort for generations to come, and offer highly personalized plans for investing, charitable giving, and other specific needs. There are some truly outstanding professionals making up the Los Angeles wealth management landscape. We’ve listed more than 40 of them here, along with some basic information about their careers, practice and a peek into what makes them so good at what they do.

Read full article here.