TACTICAL STRATEGIES

PREMIER WEALTH TACTICAL & PREMIER WEALTH TACTICAL CORE

Concerns about inflation, interest rates, and the debt ceiling have seemingly been brushed aside as investors rushed towards the Mega Cap Tech stocks chasing the allure of the AI revolution. Markets have managed to climb the proverbial wall of worry and make new highs for the year on both the NASDAQ and the S&P 500.

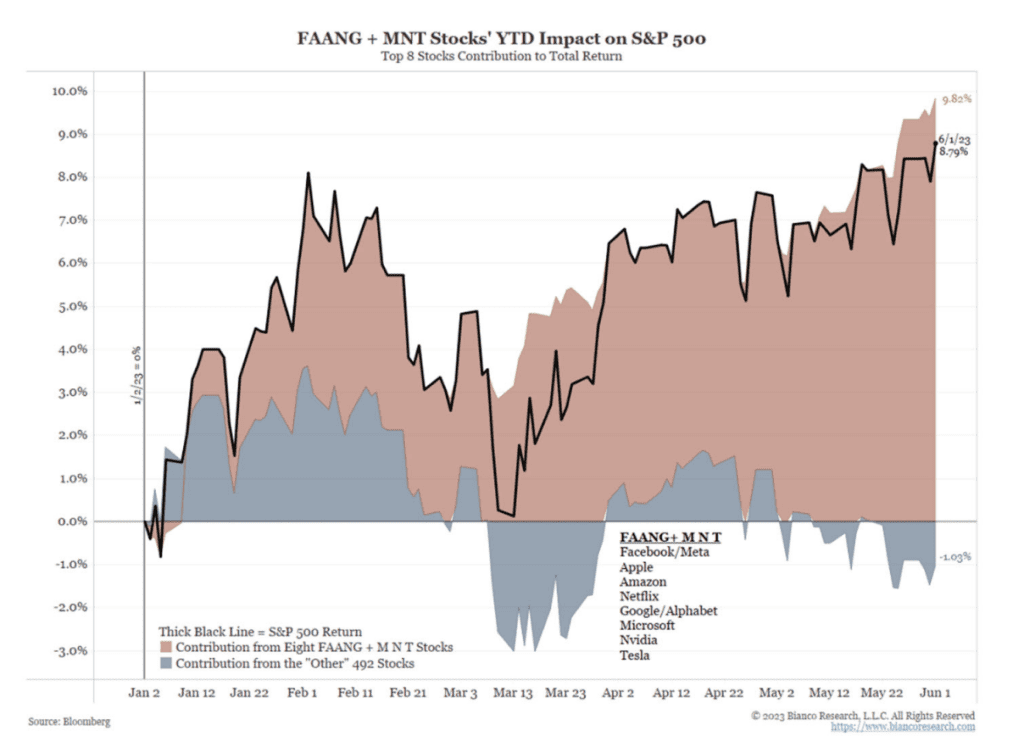

While the action in the market has been positive over the past month, one concern is the very narrow participation via Mega Cap Tech, especially AI and software companies. Through the end of May, the leadership was so narrow that the top 8 stocks by market capitalization on the S&P 500 accounted for a 9.8% return for the index. Since the S&P500 was only up 8.79% up to that point, that means the bottom 492 stocks in aggregate accounted for a 1% loss.

Historically, narrow markets are suspect, but we also know that these conditions can last a long time like we saw in the dotcom bubble. The good news is that we did see an expansion in participation as the S&P 500 broke out and made new highs last week.

Fundamentally, the combination of much better than expected earnings and the resolution of the debt ceiling appeared to be the catalyst that gave the markets the momentum to reach new highs. The messaging from the Fed that a pause in rate hikes in June likely contributed to that.

We have moved to increase our exposure and should things broaden out, more could be warranted. Some things to keep in mind is that some backing and filling should be normal, especially after the torrid run the NASDAQ has had.

In the intermediate term, the resolution of the debt ceiling means that the US will be issuing a massive amount of treasuries over the next few months. Some estimates are for more than 1 trillion before the third quarter. That would suck some liquidity out of the market.

In addition, student loan repayments are to be reinstated by September, likely reducing aggregate demand as what was temporary disposable income is forced back into paying debt.

Outside of the short term, markets will likely continue to be dictated by inflation and the Fed’s actions to fight it. While a pause is at hand, the Fed could be forced to do more if inflation doesn’t come down as expected. The strong jobs numbers we saw last week affirmed a strong labor market, which could keep inflation stickier than anticipated. In all, the technical action looks good but some caution is still appropriate as there is a confluence of factors that can still trip up this market later down the line.

TACTICAL OPPORTUNITY

Tactical Opportunity added some exposure as the market showed some life. The best month came in a rebound from AMZN, while several other stocks also had nice months. The narrow market makes it difficult to find buy signals, but we will add as they appear.

FULLY INVESTED STRATEGIES

ETF SECTOR ROTATION

The Growth sectors pressed their lead for the year with big moves over the last month in Tech (+9% vs a +3% S&P) and Consumer Discretionary (+9%). Communications (+5%) also had a good run. Outside of that, the picture was not pretty. Defensive plays Healthcare (-3%) and Consumer Staples (-6%) were the biggest laggards. Our model remains leaning toward the middle with overweights in Tech, Communications, and Energy. The action during the month saw us reduce our Healthcare exposure to an underweight.

In the broad markets, Growth posted a +6% month compared to a negative one for Value. Small Caps outperformed and Internationals lagged. Currently, we still hold exposure in Europe, but not Emerging Markets.

EQUITY GROWTH OPPORTUNITY

The market found its footing in May, led by the resurgent Technology sector. The broad indices appear to be following suit, which is increasing our optimism. We are continuing to explore increasing the beta in the portfolio to take advantage of this upswing.

EQUITY GROWTH AND VALUE

No surprise here as Tech holdings had outsized runs since May 1, such as Advanced Micro, Applied Materials, Nividia, and Broadcom. Also, as expected, defensive names lagged, though most not too badly. Normal rotating is expected to occur as the market decides if the Growth run will last.

EQUITY DIVIDEND INCOME

With Growth getting the headlines, the more value minded dividend stocks lagged, and as a group were down slightly. Healthcare and Staples stocks declined as money rushed for AI names. Not abnormal behavior for a dividend group. Normal activity expected.

RISK BLENDED STRATEGIES

Our Risk Blended Strategies are a combination of both Premier Wealth Tactical Core and ETF Sector Rotation. Please see the above commentary for more information on each strategy.

- Churchill Moderate: 70% Premier Wealth Tactical Core / 30% ETF Sector Rotation

- Churchill Moderately Aggressive: 50% Premier Wealth Tactical Core / 50% ETF Sector Rotation

- Churchill Aggressive: 30% Premier Wealth Tactical Core / 70% ETF Sector Rotation

For a full description of each strategy, please click here.

Best regards,

CHURCHILL MANAGEMENT GROUP

877-937-7110

[email protected]

** This report is meant to inform the reader of our current market opinion, which we, as professional money managers, use in our decision-making. It should be noted that stock market and bond market data are subject to varying interpretations and any one interpretation will not necessarily guarantee investment success. The information obtained from the sources specified herein and used as a basis for our current market opinion is believed reliable, but we do not guarantee the accuracy of such information. The references to specific investments were chosen based on our current market outlook, as examples representing how aspects of the market have performed and as representation of what a strategy might own. Those are included for informational purposes only and past specific investment advice does not guarantee future results.